Ask the Expert: Read this before switching your super accumulation into a pension

If you move from a super accumulation into a pension fund you must draw down a portion of super each year – here’s what you need to know.

Question 1

I will finish work when I turn 60 next year. I have enough investments outside super to fund my current living expenses.

Is it better to leave my super ($1.6 million) in the accumulation account and let the balance increase until I’m 65, or transfer it now to an account based pension when there will be an immediate mandatory draw down?

You must be in a very solid position to fund your lifestyle with investments outside super.

As you have indicated, once you turn age 60 you can access your super in full if you are retired.

If you do move your super accumulation into a pension then yes, you will be required to draw down a portion of your super each year, based on your balance and age. As shown in the below table:

However, pension funds pay zero tax on earnings, while superannuation accounts have to pay 15 per cent on their earnings.

Therefore, the after tax return for pension funds outperform super funds. With higher balances this could be significant.

You might like

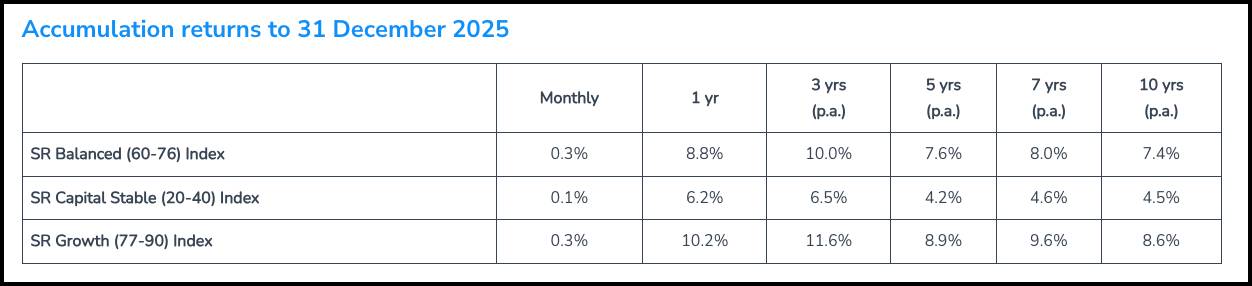

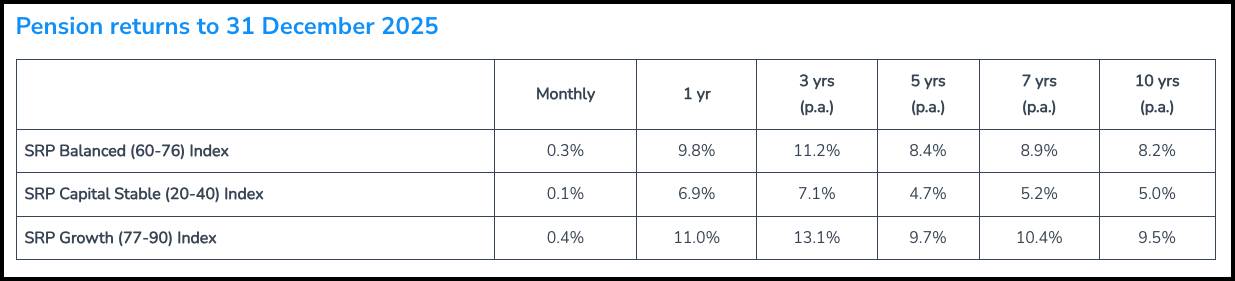

To highlight this point, have a look at the medium balanced fund returns for both super accumulation and pension funds. The pension returns are much higher, primarily because they don’t pay tax.

Source: SuperRatings estimates

Therefore, you could convert most of your super to a pension fund to enjoy the better returns – keeping a small balance in your super account.

As you receive payments from your pension – if you don’t need the money – you could then contribute them back into your super account.

Question 2

Hi Craig, my wife and I are looking at retirement in the next two years (max). We both have good super balances and are looking at moving them from the defined benefit accounts into our super pension income streams (nothing complicated).

When setting up beneficiaries we have opted to nominate each other, however in the event of something happening to the both of us (as we are travelling) are we better off having our super now and in pension stage go directly to our estate and distributed via wills?

And is this the better tax reducing option for our adult independent children

thanks

Whether the proceeds at death from your super/pension are paid directly from the super fund, or from the Estate makes little difference (just the Medicare Levy).

Stay informed, daily

When proceeds are paid to someone that the ATO doesn’t consider a beneficiary, such as adult children, 15 per cent tax is paid on the ‘taxable component’ plus Medicare of 2 per cent.

If the proceeds go to the Estate first, and they pay to the adult children, then the Medicare is not payable but the 15 per cent tax still is.

When the funds are in pension phase (income stream) there is also an option of a reversionary beneficiary, where if one spouse passes away the income stream will revert to the surviving spouse and remains in the super environment.

The above is a simplified example and other implications rather than tax should be considered. These include family provision claims if paid by estate, and the simplicity and likely quicker payment if not having to go through the Estate.

There are options available to reduce this tax by converting some of the taxable component into a tax free component. I covered that here.

It can be complicated, so I suggest speaking with your super fund or obtaining financial advice.

Question 3

We are downsizing to a unit in a retirement village. Is there anyway to avoid stamp duty?

I am told by a reputable source that you have one opportunity in your life to be stamp duty exempt.

Is this true as we have always paid stamp duty on our transactions?

Stamp Duty is a state-based tax and each state and territory has its own rules.

Mostly stamp duty exemptions or discounts are offered to first home buyers and only up to certain thresholds.

Seniors, pensioners and farmers may also be eligible for stamp duty concessions in some states, although these are less common.

Thresholds and eligibility criteria vary by location, so check with your local revenue office for specific details.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.

Want to see more stories from InDaily SA in your Google search results?

- Click here to set InDaily SA as a preferred source.

- Tick the box next to "InDaily SA". That's it.