Ask the Expert: Long term v short – choosing the right super investment settings

Question 1

I am 63 years old and intend to retire in two-three years.

Currently, due to market volatility, I have shifted my super into a cash investment option, so am experiencing lower growth.

My balance is about $570,000. Everywhere I read, the advice is to leave super in a higher growth option and to ride out any market fluctuations. However, this advice is always prefaced with “in the long term” and is pitched at people in their 40s and 50s, or younger.

What would you suggest for someone of my age and circumstances, given the current market volatility and unpredictability and the short time until I retire?

First, trying to time the market for when to switch to cash is very difficult. Then, trying to time the market to switch back into a balanced or growth options is just as difficult. Getting both decisions right is next-level difficult.

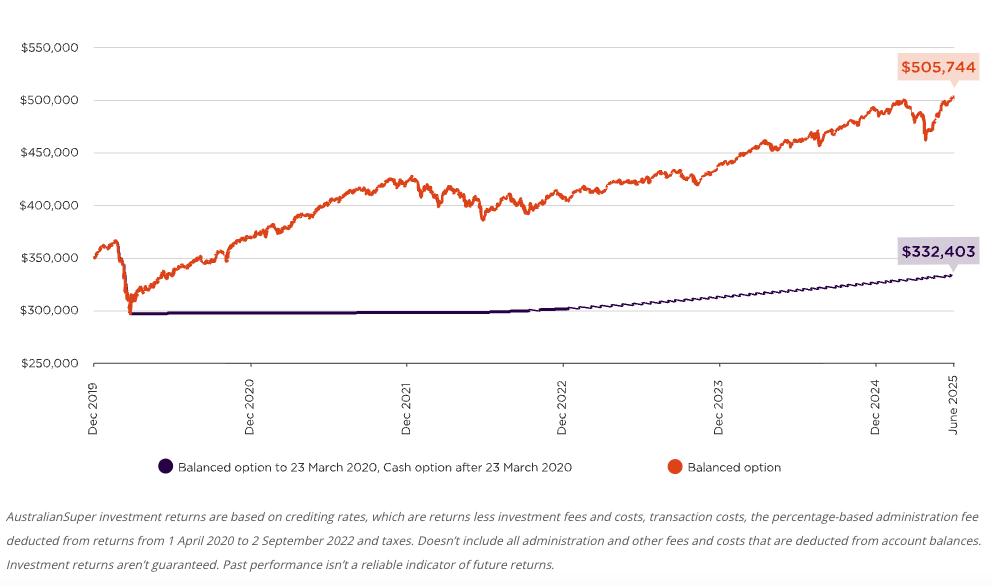

To highlight this, AustralianSuper provided the following example. It shows someone who switched from their balanced option to cash when Covid hit and markets originally crashed. As you can see, the Balanced option quickly recovered and just over five years later the difference is $173,341 (from a starting balance of $350,000).

You might like

To your next point about retiring in the next few years. A 65-year-old male can expect to live more than another 20 years, on average, i.e. 50 per cent of men will live longer than that. And women, on average, live a couple more years than men.

Hopefully you are planning for your super to last as long as you. Therefore, the majority of funds should be invested with a long-term outlook.

Speak with your super fund to identify a suitable option that matches your risk and return profile, and one you will be comfortable sticking with long term.

To put your mind at ease, you can earmark a portion of your super to retain in cash. These funds can be used in the first few years of your retirement while the majority of your funds can remain in a more suitable long-term option.

Question 2

I am 61 years old, my husband turns 70 in May. He wants to retire, I don’t.

We have our home (not paid off) and a holiday house (paid off). I have a super worth about $300,000, he has little super (about $15,000).

Stay informed, daily

If I continue to work full time, is he eligible for part pension? We still have two children at home studying at university for another two years.

Greetings to you,

Your holiday home will be asset-tested. Depending on its value, it may impact your husband’s age pension.

Your super won’t count against the age pension until you reach age 67, or unless you move in into a pension.

If your assets (holiday home, his super, bank accounts etc) are less than $481,500, then he would receive a full age pension under the assets test.

If assets are above this figure, his age pension would start to reduce. It goes to nil if assets reach $1,059,00 (note, these figures are higher if you don’t have your own home).

Your income/salary may impact his age pension.

Income of less than $380 a fortnight won’t affect his pension. After that it starts reducing. It goes to nil if your combined income is $3844.40 a fortnight.

Centrelink will apply whichever gives the lower results between the assets and income test.

It’s good that you wish to continue working. This will strengthen your financial position. It’s not just the age pension that should be focused on, but your combined income.

Hopefully your salary plus a potential part age pension for your husband is sufficient for now. If not, you could move some of your super to a transition to retirement pension to top up the income, but ideally you don’t have to and it keeps growing for your retirement.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.

Want to see more stories from InDaily SA in your Google search results?

- Click here to set InDaily SA as a preferred source.

- Tick the box next to "InDaily SA". That's it.